JANUARY 2018 ///Vol 239 No. 1

FEATURES

Eastern Mediterranean region are beginning to increase E&P activity and were able to bring several key projects on stream in 2017.

Emily Querubin, World Oil

Emily Querubin, World OilEGYPT

Egypt is home to several mega-projects—including Nooros and Zohr fields—which reportedly will double the country’s natural gas output by 2020. This year, the country is on track to end natural gas imports and become self-reliant. This is critical, as approximately 70% of the country’s electricity is powered by natural gas. “The fields of Zohr, North Alexandria and Nooros are among the most important projects that will increase natural gas production … and will contribute to [Egypt’s] natural gas self-sufficiency by the end of 2018,” said Petroleum Minister Tarek El Molla in a statement.

During 2017, Egypt’s production increased to approximately 5.1 Bcfd, from about 4.4 Bcfd the year prior. Production at Nooros field, which is found offshore the Nile Delta, hit record levels early in the year. Eni reported that the field’s seven operating wells were producing at a rate of 170,000 boed.

In December, however, Egypt’s super-giant Zohr field was brought onstream less than two-and-a-half years after discovery. Eni discovered the field, which is said to hold approximately 30 Tcf of gas-in-place, in August 2015. It is situated 120 mi north of Port Said, in water depths of more than 4,900 ft. According to Eni, 20 wells are expected to be drilled at Zohr by the end of 2019.

Eni, through its JV with Petrobel, operates the Shourouk concession, which contains Zohr field. In February 2017, BP acquired a 10% interest in the concession. Just prior to start-up in October, Rosneft also acquired interest (30%) in the field. In addition to its participation at Zohr field, BP has explored the region in recent years. The oil major has struck oil and gas throughout Egypt, including at Taurt North, Seth South, Salmon, Rahamat, Satis, Hodoa, Notus, Salamat and Atoll.

The company’s West Nile Delta (WND) development has been a key contributor to continued growth of Egyptian E&P. It is made up of five fields—Taurus, Libra, Giza, Fayoum and Raven—which stretch across two offshore concession blocks, North Alexandria and West Mediterranean Deepwater. According to BP, production from all five fields is expected to reach up to 1.3 Bcfd. This reportedly is equal to approximately 30% of Egypt’s present-day gas output. Production began at Taurus and Libra fields in March 2017, contributing an additional 600 MMscfd to Egypt’s overall output. As part of a subsea greenfield development, Taurus and Libra fields consist of nine wells—six in Taurus and three in Libra—with a 26-mi tie-back. The remaining three fields are expected to begin production in 2019. The WND development will include 12 wells and two deepwater subsea tie-backs, according to BP.

ISRAEL

While the greater part of Israel’s E&P activity continues to center around Tamar and Leviathan natural gas fields, the development of Karish and Tanin fields is quickly becoming a focal point, as well. After acquiring the fields in 2016, Energean Oil & Gas hastily submitted a Field Development Plan (FDP) for the offshore assets, which are said to hold gas resources estimated at 2.4 Tcf, plus 33 MMbbl of light hydrocarbons liquids.

The FDP includes the use of an FPSO unit, Fig. 1. According to the company, this will support maximum recovery of reserves and achieve minimal environmental impact. It will be installed nearly 56 mi from the shoreline, with a capacity of 400 MMscfd. Energean says the Karish Main Development will see three wells drilled, as well as a dry gas pipeline connection to the Israeli natural gas transmission system. Development of Tanin will follow shortly, thereafter. Six wells are planned for the area, which will be connected to the same FPSO that hosts the Karish wells.

In August, Energean reported that the FDP was approved by the Israeli Petroleum Commissioner. First gas is expected in 2020. Israel registered the highest growth in gas demand worldwide, according to BP’s 2017 Energy Outlook. Energean says that the gas produced from Karish and Tanin fields will increase supply and bring competitive prices to the Israeli domestic market.

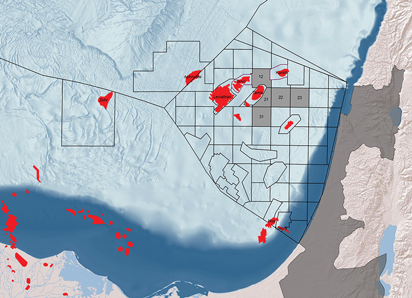

Energean increased its E&P activity offshore Israel in December, when it was awarded five additional exploration licenses in the area, Fig. 2. Accordingly, the company’s portfolio now includes 13 exploration licenses, overall. Energean says that it believes Blocks 12, 21, 22, 23 and 31 are very prospective. According to a company release, the initial exploration period under each of the new licenses is three years. If the exploration licenses result in any discoveries, the company reportedly plans to tie them back to the same FPSO that hosts Karish and Tanin.

Zion Oil & Gas also has had a promising year in Israel. In early June, the company announced that it had spudded the Megiddo-Jezreel #1 well in the Jezreel Valley, south of the Lower Galilee region. CEO Victor Carrillo said, “It has been a complicated and difficult multi-year journey to get to this point, but our entire team is very excited to see this project finally come to fruition. We anticipate drilling through at least four different geologic strata with oil and gas potential.”

Situated within the onshore portion of the Levant basin, the Megiddo-Jezreel license area is an exceedingly prospective zone. According to Zion, an independent study conducted by Beicip-Franlab in 2015 determined that up to 6.6 Bbbl of oil in-place have yet to be recovered from the basin’s offshore area. At CERAWeek last spring, Israel’s Energy Minister, Dr. Yuval Steinitz, said that because of the basin’s “substantial reserves,” Israel is now working to become a gas exporter. Development of the offshore field, however, is not anticipated for another five to 10 years. Nonetheless, when it does begin producing, Steinitz said that it likely will be competing with North Sea producers for customers in Egypt, Turkey, Italy and Western Europe.

In September, after drilling more than 9,000 ft into the subsurface, Zion announced that it obtained evidence of having penetrated hydrocarbon zones onshore. Through enhanced petrophysical analysis of its wireline logging suites, the driller’s CEO said that he believed it was “on the verge of penetrating a key zone of interest, the Triassic Mohilla Formation, [which] has produced significant quantities of oil in Givot Olam’s Meged field.” The company would not, however, speculate on the zones’ possible volume, producibility or commerciality. Details reportedly will not be released until the Megiddo-Jezreel #1 well has reached its anticipated TD of 15,000 ft.

Israel’s largest natural gas reservoir, Leviathan, made progress early last year, as well. The offshore project’s partners—Delek Group, Ratio Exploration and Noble Energy—sanctioned the first phase of development in February. As operator, Noble Energy said that the field’s initial development will involve four subsea wells, each capable of flowing more than 300 MMcfd. Production reportedly will be delivered via two 73-mi flowlines to a fixed platform, positioned about 6 mi offshore.

The field, which is said to contain 22 Tcf of gross recoverable resources, is expected to produce first gas by the end of 2019. Noble Energy Chairman, President and CEO David Stover explained, “Bringing Leviathan online will expand Israel’s supply of natural gas, further support the State’s commitment to convert coal-fired power generation facilities to cleaner-burning gas, and provide affordable energy resources to Israeli citizens and neighboring countries in the undersupplied region.”

CYPRUS/TURKEY

In the Republic of Cyprus, E&P activity continues to be slow-going. Since its discovery in 2011, Aphrodite field still awaits a final investment decision (FID). The offshore gas field, situated in Block 12 of the country’s maritime exclusive economic zone, is just 21 mi west of Israel’s Leviathan field. The block reportedly could hold anywhere from 3.6 to 6.0 Tcf of natural gas.

“The commercialization of gas remains a priority for the government,” Dr. Stelios Nicolaides, director of hydrocarbons service for the Republic of Cyprus’ Ministry of Energy, Commerce, Industry and Tourism, said during the Eastern Mediterranean Gas Conference last March. “With our partners, we have determined that the most reasonable commercial path forward is a pipeline to Egypt.” To achieve this, however, intergovernmental cooperation would be required before proceeding with construction of a new gas pipeline.

Dr. Nicolaides also explained that the Cypriot government is actively pursuing agreements with bordering states. At the time, the country had already signed framework agreements with Egypt, Greece and Lebanon for cooperation in the development of hydrocarbons in the area. Additionally, it has issued a number of offshore licensing rounds over the last several years to help promote regional E&P.

North of Cyprus, in Turkey, Condor Petroleum has continued to focus its E&P efforts on Poyraz Ridge gas field, situated on the Gallipoli peninsula, in the northwestern part of the country. In January 2017, the company announced positive drilling results at its Poyraz West 2 appraisal well. According to the company, the step-out well encountered over 465 ft of net pay, of which nearly 197 ft were of a newly discovered pre-Sogucak reservoir. It was determined that the new reservoir is older and deeper than the Gazhanedere and Sogucak intervals, which had already been assessed. The discovery significantly heightened the prospectivity of similar structures within the license area, the company said.

After drilling a total of five wells and completing the construction of a central processing facility and pipeline system, Condor announced first gas last month, in mid-December. The Poyraz Ridge central processing facility has a capacity of 15 MMscfd, and the 6-in., nearly 10-mi pipeline is tied back to the Turkish natural gas pipeline system.

Valeura Energy also announced a discovery in northwestern Turkey, in late November. The company reported that the Yamalik-1 well—which was the first well drilled under Phase 1 of its Banarli farm-in agreement with Statoil Banarli Turkey BV—was drilled to a TD of approximately 13,766 ft and subsequently would undergo a full 60-day testing program.

Valeura reported that the first of four production tests had already been completed successfully in the Kesan formation. The company says the positive test results considerably increase the odds that Yamalik-1 will be tied in after testing concludes. Summative test results reportedly will be disclosed upon completion of the testing program. The discovery follows Valeura’s first gas find with the Bati Guren-1 exploration well in January 2016, which also was on the Banarli license, in the Thrace basin, Fig. 3.

LEBANON/SYRIA

Although it is not ordinarily recognized as a particularly noteworthy region for E&P, Lebanon held its first licensing round in 2017. The offshore bidding round is the country’s ardent push to join its Eastern Mediterranean counterparts in their regional success, as they’ve reported recent oil and gas finds nearby, in Israel and Egypt. This is a particularly momentous milestone for Lebanon, considering that the auction was originally scheduled to be held back in November 2013.

When bidding closed for pre-qualified companies on Oct. 12, one consortium of oil majors had submitted bids for Blocks 4 and 9, Fig. 4. The consortium—consisting of Total, Eni International and JSC Novatek—is now committed to an exploration program, which is set to begin drilling operations in 2019.

The bidding deadline had been postponed for nearly a month, giving potential bidders more time to understand a new tax law set forth by Lebanon’s parliament. Approved in September, just weeks before the deadline, the law mandates that regional oil revenue be taxed. It has been reported that domestic and geopolitical problems have caused a delay in the country’s energy auctions for years, and the country is in need of the additional revenue to curb debt.

In neighboring Syria, continued military discord and economic sanctions prove detrimental to regional E&P. Due to the ongoing conflict, the EIA reported that Syria’s production of petroleum and other liquids plummeted to approximately 35,000 bpd in 2016. Although it reportedly produces less than 0.05% of the global petroleum supply, a U.S. cruise-missile attack on the country shook financial markets in early April. This was largely due to its proximity to Iraq, OPEC’s second-largest producer.

Futures in New York and London rose more than 2%. “It seems [the] spike is just a knee-jerk reaction to the missile strike,” Thomas Pugh, a commodities economist at Capital Economics, told Bloomberg. “Syria produces little oil itself, so the spike probably reflects the risk of increased tensions between the U.S. and Russia or Iran.”

In July, it was reported that the Syrian army was able to take control of a number of oil wells in southwest Raqqa province from Islamic State militants. Backed by Iranian militias, the army reportedly seized Wahab, al Fahd, Dbaysan, al-Qseer, Abu al Qatat and Abu Qatash fields, as well as several villages in the area. The raid followed a reported strike in the central province of Homs, east of Palmyra, where the army struggled to regain control of Arak and Hail gas fields.

GREECE

While Greece continues to focus heavily on exploration in the Gulf of Kavala’s Prinos basin, the country is beginning to see E&P activity elsewhere, as well—primarily in the western region.

Although a large portion of Greece’s E&P activity takes place offshore, 2017 saw several key developments in its onshore blocks. In March, Energean Oil & Gas, which is the country’s chief hydrocarbon producer, agreed to farm out a 60% interest in its Ioannina and Aitoloakarnania Blocks to Repsol, Fig. 5. Repsol also took over operatorship of the blocks, found in the western region of the country. According to a release, Repsol plans to acquire a 2D seismic survey over the Ioannina Block in the next year. Subsequently, the company plans to carry out an FTG and a 2D seismic survey over Aitoloakarnania Block. The blocks, which cover an area of 8,547 km2, are said to be “priority exploration targets for Energean and strategically important for the Greek oil and gas sector.”

In September, Energean was granted government approval to begin the development of Katakolo field, also in western Greece. The $50-million FDP, which was submitted in February, includes multiple extended-reach wells. It will target approximately 11 MMboe that has remained undeveloped since its discovery in the early 1980s. Drilling is expected to begin in 2019, and first oil is anticipated for 2020. ![]()

http://www.worldoil.com/magazine/2018/january-2018/features/regional-report-eastern-mediterranean

I see you don’t monetize your website, don’t

waste your traffic, you can earn extra cash every month because you’ve got hi quality content.

If you want to know how to make extra bucks, search for: Mertiso’s tips best adsense alternative